Saturday, November 6, 2010

Woop woop! Guynance is moving!

Though I hooked up the domain name a while ago, I finally actually moved the site over to Guynance.com. So now there are pictures! And shirts cometh! And it no longer looks like a site made by a 6 year old in the late 90s (now it looks like it was made by a 12 year old in the early 2000s, baby steps)!

Thursday, November 4, 2010

So the credit companies think you are a worse risk than Mike Tyson eh?

Sorry it has been so long, CFA level 3 studying has started and it is vampiring my time. For this post i'm experimenting with a new form of media! I'm still giggling like a school girl about this one:

Guynance: Goin straight nuts on your minds lady parts the video

Guynance: Goin straight nuts on your minds lady parts the video

Thursday, October 14, 2010

A "Currency war" sounds about as intimidating as a gang of puppies with bandanas and tear drop tattoos...what's the BFD?

I know! I promised! Way back in the black n white film era of mid August 2010, I wrote an intro post saying that this blog would be able to give you some sort of response to some dweeb saying “the fed is sacrificing the dollar like a virgin in Tecnochtitlan” other than your usual response of “NEEERRRRRRDDDDDDDDD.” So let’s start from the top, the first question I got on this was “uhhh….bro….what the shit is Tech…notch….tit….land?” it was the capital city of the Aztec civilization, founded in 1325, and they did not take too kindly to virgins there. So now from the top that’s a little…less…at the top…than that top, currencies: what they are, how their value changes, why different interest groups want to control their values, and how they are effing up the current international economic situation.

At their most basic level, currencies are what you use to buy shit in a different country. You’re chillin in Canada and you wanna buy some knock off Big Wrrrreeague Chew from South Korea, but they don’t want your stupid Canadian monopoly money they want to be paid in South Korean Won (most of you were probably expecting a China joke there, and trust me I had it all written and everything, but China’s currency policy is super important and all messed up so its got its whole own section later….engrish included). So you click in your monacle, iron your tuxedo t-shirt and roll down to your local financial institution to hook up some damn Won! At the same time you are doing this, another gender neutral person across town is looking at investing some money super low risk and notices that government bonds in South Korea will pay it 3% per year instead of 0.75% in Canada and says “screw this noise, I’m gonna give the South Korean government my cashish instead” and travels to their financial institution to hook up some Won as well. In both of these situations you are getting rid of or “selling” Canadian Dollars and “buying” South Korean Won. So what happens when everyone is selling something and buying something else? The price of the desired object rises (ISBA: currency “appreciates” when it goes up in value).

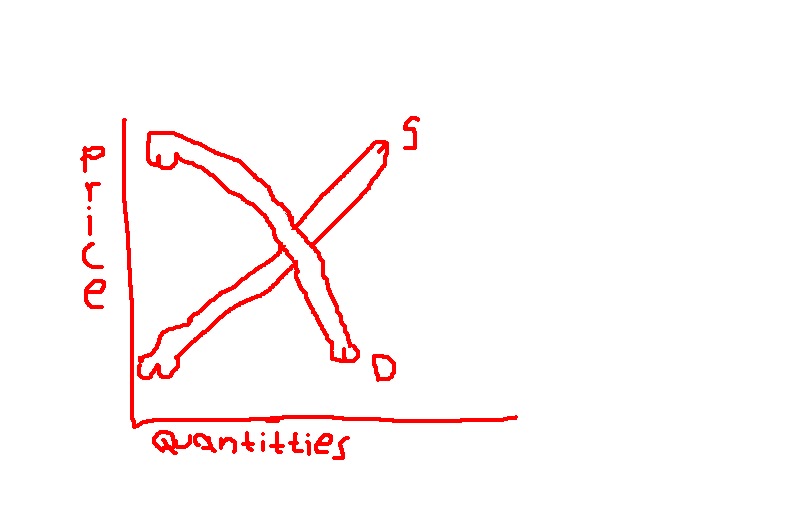

Currencies can kinda be thought of as similar to anything else in that it’s “price” is controlled by supply and demand. Think back to economics 101…thiiiiiiiiiink…...look past the girl with the playboy bunny trampstamp you can just see through her chair, forget about the guy with the….sexy thing that…some guys have…or whatever, and remember this diagram:

Dude.……..your economics teacher was pretty fucked up….. I guess we can work with this though?

So if demand (downward sloping boner) goes up while supply (upward sloping boner) remains the same, price goes up and that makes it more expensive relative to other currencies. Demand decreases while supply remains constant, price goes down. Supply goes up without an increase in demand, the price of the currency goes down and vice versa.

So we touched above on a few of the things that can happen to drive demand and therefore increase currency values, but for those who can only learn things in list form here’s a summary:

China

The US

And so we come to the crux of this “currency war” that the main stream media is spazzing out about. The US, and a lot of the rest of the world, wants China to allow their currency to increase in value because Chinese exports and thus US imported goods like toasters, condoms, and politeness are artificially cheap and that is crowding out other emerging markets from exporting. China and other emerging markets want the Americans to raise interest rates and stop jooking their currency so that money doesn’t flood into these emerging markets and drive their values up, hindering their exports. The Bank of Japan has already stepped in to decrease the value of its currency and many other emerging market governments are talking shit about doing the same. It is a race to the bottom and no one will be the winner in the end.

I know there was a veritable ocean of information just assaulting your grill, but it was necessary. That’s the thing about macroeconomics, it’s impossible to write about one thing in isolation because everything is connected. I sit down to write a nice little article and then boom next thing you know I go into an economics blackout and wake up 3 days later in a pile of Google searches, covered in mustard with a 3000 word post and Bobby Banker saying "really dude? dicks made in paint for the supply and demand?". It’s a rough life. Seriously though, this is one of the biggest topics out there this currency war:

- U.S. is currency war's tomb maker: China economist | Reuters (October 14)

- IMF warns against currency war - Reuters (October 10)

- Dollar falls as 'currency war' concerns linger (October 11)

- BBC News - IMF chief's warning of currency war 'real threat' (October 7)

The best hope for sanity seems to be the upcoming G20 meeting in November, where ideally both sides can come to some sort of compromise that will allow for a narrowing of China and the US's trade imbalances (surplus and deficit). There is no easy answer, but countries acting alone to try and protect themselves and their exports is a surefire way for disaster, the only answer is cooperation.

At their most basic level, currencies are what you use to buy shit in a different country. You’re chillin in Canada and you wanna buy some knock off Big Wrrrreeague Chew from South Korea, but they don’t want your stupid Canadian monopoly money they want to be paid in South Korean Won (most of you were probably expecting a China joke there, and trust me I had it all written and everything, but China’s currency policy is super important and all messed up so its got its whole own section later….engrish included). So you click in your monacle, iron your tuxedo t-shirt and roll down to your local financial institution to hook up some damn Won! At the same time you are doing this, another gender neutral person across town is looking at investing some money super low risk and notices that government bonds in South Korea will pay it 3% per year instead of 0.75% in Canada and says “screw this noise, I’m gonna give the South Korean government my cashish instead” and travels to their financial institution to hook up some Won as well. In both of these situations you are getting rid of or “selling” Canadian Dollars and “buying” South Korean Won. So what happens when everyone is selling something and buying something else? The price of the desired object rises (ISBA: currency “appreciates” when it goes up in value).

Currencies can kinda be thought of as similar to anything else in that it’s “price” is controlled by supply and demand. Think back to economics 101…thiiiiiiiiiink…...look past the girl with the playboy bunny trampstamp you can just see through her chair, forget about the guy with the….sexy thing that…some guys have…or whatever, and remember this diagram:

Dude.……..your economics teacher was pretty fucked up….. I guess we can work with this though?

So if demand (downward sloping boner) goes up while supply (upward sloping boner) remains the same, price goes up and that makes it more expensive relative to other currencies. Demand decreases while supply remains constant, price goes down. Supply goes up without an increase in demand, the price of the currency goes down and vice versa.

So we touched above on a few of the things that can happen to drive demand and therefore increase currency values, but for those who can only learn things in list form here’s a summary:

- If a company has attractive products to sell internationally (oil and other natural resources, knock off big league chew, etc), it will generally export more than it imports (ISBA: countries that do this are said to be running a “trade surplus” or a “trade deficit” if they import more than they export). Say this is South Korea, more people from other countries will buy the Won than people in South Korea selling the Won, and it will become more expensive.

- If a country has a more attractive interest rate for investors in the government bond market, they will flock to get that currency to be able to invest in that country’s bonds. This also applies if there is just a better investment climate in certain countries (ie. “Everything sucks here, but there are some gnarly companies to invest in/acquire in South Korea let’s get some Won and go to town”)

- The relationship between interest rates is actually super exact in theory. If a country’s interest rate is 2% higher than another, its currency SHOULD appreciate 2% against that other country over a year. This is called the (ISBA) International Fisher Effect. If you can use this one accurately in conversation you have my blessing to chug and spike whatever you are drinking, yell “spring break Panama City 2004”, and promptly exit the room for you have hit the high water mark of your night, financial conversationally speaking.

- This final major factor driving currency values higher is a less logical one and more of an emotional response: the flight to safety. This essentially happens when you have terror poos, stop caring about return, and hunker down with whatever you think won’t totally collapse. This is one of the things keeping the US dollar afloat these days.

- Well what causes the SUPPLY of money to INCREASE?? Eh? EH? See? All these articles hang together in the grand scheme of things! For those of you looking at me cockeyed, monetary policies like decreasing interest rates and quantitative easing cause a large increase in the supply of money (see stimulus article for deets), which in turn will drive the value of a currency down.

- An offshoot of these monetary policies that expand the supply of money (ISBA: “expansionary monetary policies”) is inflation. There is a complicated explanation for why this erodes a currencies value but if you just think about it from a sensical perspective, if one Canadian dollar buys less in Canada…. why would someone else pay the same amount as they did before to acquire that one Canadian dollar? The only thing to remember here is that currencies are relative though, so if Canada has 5% inflation and the other country also has 5% inflation…. then the currencies won’t change against one another.

- A country running a trade deficit will also de-value the currency (as discussed above).

China

- Everything described above? That all applies to floating rate currencies. Which are currencies whose value can change along with market forces. However, some countries elect to have a fixed (ISBA: “pegged”) currency, which uses the USD as a peg. China is one of these countries. If the USD rises then the Yuan (a.k.a. the Renmibi… I know! It sounds Italian, just go with it) rises and vice versa. The goal of this is to make international trade more consistent and predictable by having a relatively stable exchange rate. The way they do this is by the Chinese central bank saying “oh harrrroowwww market forces how you?” then proceeding to use their gigantic foreign exchange reserves to do the opposite of every effect of the market. Too many people buying Chinese goods or investing in China? Boom, buy some more USD and sell their own currency into the open market to increase supply and reduce the value again.

- It is the United States and much of the rest of the world’s opinion that the Yuan is significantly lower than it should be and this makes China’s exports super cheap internationally speaking. This makes sense if you think about it cause if the Yuan is held artificially low, then one dollar will buy more stuff in China than it will in say South Korea if the Won is correctly valued. Who are you gonna buy from then right?

- So sounds ok in theory right? The problem with pegs is that they are a bitch to maintain. If the for realsies value of your currency gets too far out of whack with the peg and you don’t have enough foreign currency to maintain the peg then your currency can revalue a shitload all at once and all kinds of hell breaks loose. This happened in Thailand in ‘97 and the Thai currency depreciated 30% almost instantly. It has also happened fairly recently in Russia (’97), Mexico (’95), and Argentina in 1999. (argentina debt crisis as well). China, though, has gigantic USD reserves and so has no trouble maintaining this peg, though they are under a buttload of international pressure to allow the Yuan to appreciate to even the playing field.

- Because China has such a gigantic amount of American currency (USD 2.45 Trillion as of March 2010), they have the power to eff with the value of the USD as well as their own currency…. needless to say this has important people in the States terrified.

The US

- The US is special because the value of its currency isn’t only derived from what happens in the US. It is the (ISBA) international reserve currency, which means basically that all governments hold it as their foreign exchange reserve and all of the commodities (gold, oil, corn, grain, etc) are priced in it. This means that there will ALWAYS be more of a demand for this currency than others, so a TON more of it can be created and sloshing around before the value of it is significantly deteriorated. Also, it has the benefit of being the currency that everyone flocks to when the proverbial poop hits the rapidly rotating device, further propping up its value in times of crisis.

- This being said, in my opinion the US Federal Reserve is doing its damn best to introduce the USD to its friend Throat Opener Charlie. US interest rates are at 0% and Quantitative Easing (see last post on stimulus) have taken the effective interest rate into negative territory (did your head just explode a teensy bit there? Yes essentially the US is paying banks to take money) and the USD, despite all its advantages is at a 15 year low against many major currencies.

- So what does a low US dollar do then? Well guess what stocks are valued in? USD. If Big League Chew Inc is trading at 5 bucks US when the USD is worth “1” (in reality it would be quoted against another currency like the Euro or the Yen or something but for illustration purposes), then Big League Chew Inc is gonna be trading at 10 bucks US if the USD is worth 0.5 no? So what distracts from a financial crises better than “S&P up 40% on the year!! Recovery in full swing!!” Take a look at this tasty little nug:

- Note: I would have loved to have made another wiener chart but alas sometimes real data works better. The blue line is the S&P 500, which essentially represents how the 500 biggest stocks on the New York Stock Exchange are doing (ISBA: the S&P 500, NASDAQ, and things like that are called “indices” or an “index”). The green line is an ETF that tracks the value of the USD. Notice that generally when the green line is going down the blue line is going up? Not a bad way to help it seem like everything is panda babies and rainbows eh? Again there are a TON of other factors that go into determining the price of an index like this, but this is a pretty strong correlation.

- A low USD also discourages Americans from buying foreign shit (cause it becomes super expensive) and encourages foreigners to buy American shit (cause it becomes super cheap).

- The bitch of a shitty USD though, is that because the returns are so crappy (0% interest rates don’t exactly make for a great return on American government bonds) and there is soooo much money sloshing around, a ton of money is flowing into emerging markets, where the returns will be much higher. Because people need to get the currency of those emerging markets to get these bonds, their currencies are flying upwards in value and guess what? No one wants their exports anymore cause now they are expensive and their fucked.

- The bottom line is that the Americans can keep printing currency as long as the USD is the international reserve currency. The USD will remain the international reserve currency for the foreseeable future because there is no alternative. It is in China’s interest that the value of the USD remain high, because they have so many in their reserve, however if the value of the USD is high, the value of the Yuan will rise due to the peg, which is not in China’s interest.

And so we come to the crux of this “currency war” that the main stream media is spazzing out about. The US, and a lot of the rest of the world, wants China to allow their currency to increase in value because Chinese exports and thus US imported goods like toasters, condoms, and politeness are artificially cheap and that is crowding out other emerging markets from exporting. China and other emerging markets want the Americans to raise interest rates and stop jooking their currency so that money doesn’t flood into these emerging markets and drive their values up, hindering their exports. The Bank of Japan has already stepped in to decrease the value of its currency and many other emerging market governments are talking shit about doing the same. It is a race to the bottom and no one will be the winner in the end.

I know there was a veritable ocean of information just assaulting your grill, but it was necessary. That’s the thing about macroeconomics, it’s impossible to write about one thing in isolation because everything is connected. I sit down to write a nice little article and then boom next thing you know I go into an economics blackout and wake up 3 days later in a pile of Google searches, covered in mustard with a 3000 word post and Bobby Banker saying "really dude? dicks made in paint for the supply and demand?". It’s a rough life. Seriously though, this is one of the biggest topics out there this currency war:

- U.S. is currency war's tomb maker: China economist | Reuters (October 14)

- IMF warns against currency war - Reuters (October 10)

- Dollar falls as 'currency war' concerns linger (October 11)

- BBC News - IMF chief's warning of currency war 'real threat' (October 7)

The best hope for sanity seems to be the upcoming G20 meeting in November, where ideally both sides can come to some sort of compromise that will allow for a narrowing of China and the US's trade imbalances (surplus and deficit). There is no easy answer, but countries acting alone to try and protect themselves and their exports is a surefire way for disaster, the only answer is cooperation.

Tuesday, October 5, 2010

Official Blog Logo release

.png)

Woop woop! I made a logo!! It's been hidden as my profile pic for a few days now, but here is it's grand unveiling. Shirts are being made with this on the front and the tagline "Goin straight nuts on your mind's lady parts" on the back, if you are interested in one fire something in the comments and i'll get in touch with you somehow (I'll try and make it sound more sketchy next time i promise).

Also, now that a few posts have been made and a few people have started reading, I wanted to tell people to start damn commenting! If you liked something and want more hollaaaa, if you have a suggestion for a topic or want clarification on something speak up, if you'd like to tell me that i'm a poor writer but an amazing alchemist for I seem to have learned how to turn poo into paragraphs go ahead, and if I fucked something up call me out on it. I am not the grand imperial wizard of finance by any stretch of the imagination, just make sure to be constructive. I am open to explaining/debating shit and trust a brotha I'll write back.

Finally, big ups to everyone who has stopped by so far, I love doing this shit and you'd better love reading it. More to come.

Stay classy and keep it outta your mouth.

Monday, October 4, 2010

Stimulus sounds like what an unlucky soul provides to a gentleman prior to a pornographic movie, so what is it doing in EVERY financial headline in the last 3 years?

Ok enough of this personal finance hoohah, you wanna be able to hang conversationally with those suave sons of bitches you see on TV with their ironed clothes and matching socks. Stimulus has been probably the biggest overarching news topic in the financial news (hell even the biggest in the mainstream news) since the meltdown of 2008 had government officials and investment bank CEOs collectively committing Hari Kari (I’ll come back to try and explain the financial crisis in a later post….possibly using hooker analogies).

So we’ll focus on the main type of stimulus that governments traditionally have available to them (ISBA: stimulus bullets). I was going to write more about other types of ‘mulus, but I don’t want people to have to break out their eyelid kickstands so I’ll come back to it in a later post and stay more general for now. But first a brief interlude to discuss how banks work:

- In their simplest form banks take in some dollarz as deposits and lend those deposits out to some fools. Ideally, banks want to lend out every penny they take in as deposits because they are making interest on it. Obviously this is not feasible, because people want to, you know, withdraw their money sometimes n stuff and so the bank needs to have some cash on hand to service these people (stop giggling). So let’s say a bank takes in 100 bones in deposits (that’s dollars for those of you unskilled in ebonics) and is required to keep 10% of that in reserve (ISBA: “required reserve ratio”, 10% is approximately the required reserve ratio in North America) so they lend out 90 bucks to people who then deposit that into another bank. Then that other bank now has 90 bucks in deposits (so 190 in total deposits between the two banks), they need to keep 10% (90 * 0.1 = 9) on hand so have 81 dollaz to lend out. So now there is (100 + 90 + 81 = $279) in deposits all from the original 100 dollars, and it goes on and on and on. With a reserve ratio of 10%, the amount of money sloshing around will end up being 10 times the amount that is physically there (1000 bucks in this case). Now as long as everyone trust that the banks are good for your deposits, everything works just merrily, but the second doubt creeps into a depositor’s head that the bank might not have your money…. Well watch the fuck out. Everyone runs to the bank clamoring for their money so that they can put it in their mattress. But each bank only has 10% of the money required…. and long story short the economy is replaced with spiders. Think of it like a blow up doll. The economy is the blow up doll, the banks are the blow..up..machine…thing, and the air is trust. So what do you get when the trust evaporates? A big flaccid economy that’s what.

- The most common stimulus bullet is lowering the rate at which the central bank of every country lends money short term (overnight) to the country’s major banks (ISBA: target overnight rate). This has the effect of lowering the rates that businesses and consumers alike can borrow money from their banks, so mortgages are easier/cheaper to get, personal lines of credit are less expensive, loans for businesses to finance expansion are less expensive, and credit flooooooowwwwwsssss. Sounds gnarly right? Well for a while it is, money is “cheap” to get for the bank, so they relax their risk tolerances cause hey if someone fucks up on this loan fuck it we got bajillions more and it’s not like this money cost us much anyways, so banks start lending to people who aren’t worthy of it annnnnndd…….super simplified version of mortgage crisis of 2008 anyone? The OTHER effect of this money multiplication effect from above is, as long time readers of this blog will recall, what does an increase in the supply of money do? Wild ass inflation.

So stimulus is basically crack for the economy. It’s designed for when shit hits the fan to make people start spending again, to make banks start lending again, companies start hiring again, discourage that craaaazy notion that “saving” is good, and to generally “fix” the economy. But let me ask you this, has crack ever fixed anything long term? (Hint: no. See: the 80s). Crack gives you the ability to do backflips, befriend unicorns, and feel no pain for like 3 hours (note: that is my sheltered suburban idea of what crack doing is), but it certainly doesn’t empower you. You are more likely to wake up upside down against a wall mid somersault with your pants gone than in a responsible position. Even mainstream media likes to refer to stimulus as “the punchbowl” and uses the hangover analogy for when it is removed. Stimulus delays pain and tries to mask economic downturns with massive government spending to replace the lack of private sector and consumer spending. But the government can’t spend forever and when the crack party is over you are left with a buttload of government debt that needs to be paid off by….. taxpayers generally, through higher taxes down the road (like when your kids are all growned up) or inflation (see earlier post on the Weimar republic). But that’s another administrations problem right?

So now that I’m firmly seated on my high horse judging the work of people with MBAs and decades of experience in macroeconomics, let’s look at the alternative to stimulus. So shit hits the fan, the markets smell worse than a homeless person fart drifting through an onion, banks are freaking out and not wanting to lend to anyone, companies are laying people off left right and center, puppies are crying, and…. Well that’s it….. If the government doesn’t step in and do something about it then this is the reality. Unemployment will go up, households will cut their spending and save more, interest rates will go up because it’s riskier to lend to these new jobless consumers, and life will straight up suck… for a short period of time. Consumers and businesses, having cut spending to the bone start to have more cash, which makes them more creditworthy, which makes banks, who also have tons of cash sitting around (cause they haven’t been lending), more likely to lend, which allows businesses to expand and hire people and so on and so on. It’s the business cycle, and left to its own devices it will always return to a kind of middle point. Government policy is designed to smooooooth out the cycle and make the crashes less painful and the upswings less drastic (remember governments can raise interest rates too when things start getting too crazy). The thing is…. think about everything….yes, all of the things you know, somehow they all fit into the economy and some group of dorks at the government have to decide based on a bajillion indicators when to raise rates and lower rates and guess what? They fuck it up all the time and can actually end up making the swings wayyyyy worse.

There is no right or wrong answer when it comes to stimulus, whether it is better to just kick it old school like Dr. Dre and let the market run its course and deal with the political and social backlash of having people unemployed and poor, though for a relatively short period of time. Or is it better to manage the shit out of that shit and risk deferring all of today’s hardships onto our kids and, maybe more importantly to leaders, a future government who will have to deal with the political backlash. The Americans are deep into the manage the shit out of that shit camp right now and have racked up a truly ball shattering debt that no one really knows how they will pay off. Canada tried to say no to stimulus when Harper said “hey….we’re cool guys we already got some shit goin on don’t sweat it!” in December, 2008. The rest of the government promptly tried to form a coalition and topple him. Now Canada’s debt is mounting, but our economy has outperformed much of the rest of the world. Is this a divisive issue? Fuck. Yes. The moral of the story is: shit has to happen eventually, life financially can’t be rosy forever, but choosing suffering now over someone else suffering later is often a decision too damn hard for people only thinking in 4 or less year intervals.

So we’ll focus on the main type of stimulus that governments traditionally have available to them (ISBA: stimulus bullets). I was going to write more about other types of ‘mulus, but I don’t want people to have to break out their eyelid kickstands so I’ll come back to it in a later post and stay more general for now. But first a brief interlude to discuss how banks work:

- In their simplest form banks take in some dollarz as deposits and lend those deposits out to some fools. Ideally, banks want to lend out every penny they take in as deposits because they are making interest on it. Obviously this is not feasible, because people want to, you know, withdraw their money sometimes n stuff and so the bank needs to have some cash on hand to service these people (stop giggling). So let’s say a bank takes in 100 bones in deposits (that’s dollars for those of you unskilled in ebonics) and is required to keep 10% of that in reserve (ISBA: “required reserve ratio”, 10% is approximately the required reserve ratio in North America) so they lend out 90 bucks to people who then deposit that into another bank. Then that other bank now has 90 bucks in deposits (so 190 in total deposits between the two banks), they need to keep 10% (90 * 0.1 = 9) on hand so have 81 dollaz to lend out. So now there is (100 + 90 + 81 = $279) in deposits all from the original 100 dollars, and it goes on and on and on. With a reserve ratio of 10%, the amount of money sloshing around will end up being 10 times the amount that is physically there (1000 bucks in this case). Now as long as everyone trust that the banks are good for your deposits, everything works just merrily, but the second doubt creeps into a depositor’s head that the bank might not have your money…. Well watch the fuck out. Everyone runs to the bank clamoring for their money so that they can put it in their mattress. But each bank only has 10% of the money required…. and long story short the economy is replaced with spiders. Think of it like a blow up doll. The economy is the blow up doll, the banks are the blow..up..machine…thing, and the air is trust. So what do you get when the trust evaporates? A big flaccid economy that’s what.

- This type of rush to remove money from a bank is called a (ISBA: “Bank run”) and is almost always present to some degree in every giant market crash. The market crash of 1929 caused a number of smaller banks to fail and this trickle effect and the evaporation of trust lead to several widespread banking crises. After this, in the 30s, North American governments came up with several mechanisms to prevent runs on banks such as deposit insurance for everything under 100K. But, bank runs, like herpes, are vicious little bastards with staying power and can evolve. 2008 saw its own version of a bank run, which will be discussed in a later post.

- The most common stimulus bullet is lowering the rate at which the central bank of every country lends money short term (overnight) to the country’s major banks (ISBA: target overnight rate). This has the effect of lowering the rates that businesses and consumers alike can borrow money from their banks, so mortgages are easier/cheaper to get, personal lines of credit are less expensive, loans for businesses to finance expansion are less expensive, and credit flooooooowwwwwsssss. Sounds gnarly right? Well for a while it is, money is “cheap” to get for the bank, so they relax their risk tolerances cause hey if someone fucks up on this loan fuck it we got bajillions more and it’s not like this money cost us much anyways, so banks start lending to people who aren’t worthy of it annnnnndd…….super simplified version of mortgage crisis of 2008 anyone? The OTHER effect of this money multiplication effect from above is, as long time readers of this blog will recall, what does an increase in the supply of money do? Wild ass inflation.

- If you just woke up from a fear coma at the sight of numbers, just know that the risks of lowering the target overnight rate are that inflation will increase because the amount of money in the system increases and the easy access (ISBA: cheapness) of money could lead to a bunch of jamooks being approved for loans they can’t afford (note: that is not a racial term. Urban dictionary defines it as “A clumsy loser who is incapable of doing normal human tasks”, just wanted to free myself up to use it in future).

- But you can only cut rates to 0% right? So what if you REALLY sucked it hard and you need to go farther than essentially giving away free money?? Well that is the state that the US is in right now and it is called quantitative easing (ISBA: “QE”). In a super-nutty shell, QE is the government juicing up their account with money they made out of nothing and giving it directly to the banks to give them more to lend.

- BIIIIIG ISBA: The government using interest rates and QE to manipulate the amount of money in the economy is referred to as “monetary policy” as opposed to “fiscal policy” which will be discussed in a later post.

So stimulus is basically crack for the economy. It’s designed for when shit hits the fan to make people start spending again, to make banks start lending again, companies start hiring again, discourage that craaaazy notion that “saving” is good, and to generally “fix” the economy. But let me ask you this, has crack ever fixed anything long term? (Hint: no. See: the 80s). Crack gives you the ability to do backflips, befriend unicorns, and feel no pain for like 3 hours (note: that is my sheltered suburban idea of what crack doing is), but it certainly doesn’t empower you. You are more likely to wake up upside down against a wall mid somersault with your pants gone than in a responsible position. Even mainstream media likes to refer to stimulus as “the punchbowl” and uses the hangover analogy for when it is removed. Stimulus delays pain and tries to mask economic downturns with massive government spending to replace the lack of private sector and consumer spending. But the government can’t spend forever and when the crack party is over you are left with a buttload of government debt that needs to be paid off by….. taxpayers generally, through higher taxes down the road (like when your kids are all growned up) or inflation (see earlier post on the Weimar republic). But that’s another administrations problem right?

So now that I’m firmly seated on my high horse judging the work of people with MBAs and decades of experience in macroeconomics, let’s look at the alternative to stimulus. So shit hits the fan, the markets smell worse than a homeless person fart drifting through an onion, banks are freaking out and not wanting to lend to anyone, companies are laying people off left right and center, puppies are crying, and…. Well that’s it….. If the government doesn’t step in and do something about it then this is the reality. Unemployment will go up, households will cut their spending and save more, interest rates will go up because it’s riskier to lend to these new jobless consumers, and life will straight up suck… for a short period of time. Consumers and businesses, having cut spending to the bone start to have more cash, which makes them more creditworthy, which makes banks, who also have tons of cash sitting around (cause they haven’t been lending), more likely to lend, which allows businesses to expand and hire people and so on and so on. It’s the business cycle, and left to its own devices it will always return to a kind of middle point. Government policy is designed to smooooooth out the cycle and make the crashes less painful and the upswings less drastic (remember governments can raise interest rates too when things start getting too crazy). The thing is…. think about everything….yes, all of the things you know, somehow they all fit into the economy and some group of dorks at the government have to decide based on a bajillion indicators when to raise rates and lower rates and guess what? They fuck it up all the time and can actually end up making the swings wayyyyy worse.

There is no right or wrong answer when it comes to stimulus, whether it is better to just kick it old school like Dr. Dre and let the market run its course and deal with the political and social backlash of having people unemployed and poor, though for a relatively short period of time. Or is it better to manage the shit out of that shit and risk deferring all of today’s hardships onto our kids and, maybe more importantly to leaders, a future government who will have to deal with the political backlash. The Americans are deep into the manage the shit out of that shit camp right now and have racked up a truly ball shattering debt that no one really knows how they will pay off. Canada tried to say no to stimulus when Harper said “hey….we’re cool guys we already got some shit goin on don’t sweat it!” in December, 2008. The rest of the government promptly tried to form a coalition and topple him. Now Canada’s debt is mounting, but our economy has outperformed much of the rest of the world. Is this a divisive issue? Fuck. Yes. The moral of the story is: shit has to happen eventually, life financially can’t be rosy forever, but choosing suffering now over someone else suffering later is often a decision too damn hard for people only thinking in 4 or less year intervals.

Tuesday, September 21, 2010

Reader question: Whenever some suit starts yammering about RRSPs and TFSAs I just wanna be like yo SmyDCK, am I right? eh? EH?

You know what’s lame? Like super lame? Like lamer than getting caught peeing in public at 3 in the afternoon when you’re sober and 25? Taxes. Sure we all recognize that taxes are necessary for the government to like… govern…. and build shit… and whatever….. but fuck that noise someone else can pay THOSE taxes right? Well the government agrees….sort of. So they hooked us up with what are known as tax advantaged accounts. You still gotta pay taxes…. just less of em. This article centers on the Canadian version of these accounts, but most countries have some variety of this goin on.

Well it goes like this; you go to work with your lunchpail and your short sleeved dress shirt, stuff yourself in your work box, chuckle at Dagwood Bumstead's latest antics, slang some mild sexual harassment at the sultry new secretary, go to the women’s washroom and talk about feelings n’ shit, try to break the glass ceiling, and bring home the bacon cause you are a strong independent lioness woman! You get your bi-weekly paycheque ($2,500 from $60,000 annually), the government hops in and hustles 35% in a canvas sack with a dollar sign on it ($875) and boom bam baby it’s saving time with the rest ($1,625). After paying off your monthly installment on the platinum edition sex swing, you toss $250 into a well diversified RRSP filled with ETFs and sit back feeling pretty damn good about yourself…. So where the shit are the tax advantages you should be asking yourself at this point?

Well my friend, when tax season rolls around at the end of the year and you are crushing wine and filling out your taxes with your sexy tax glasses on, you get to deduct all that money that you put into your RRSP from your annual taxes. So, break out your abbacus, say you paid off the swing and were able to maintain contributing $250 every two weeks, so $500 a month * 12 months = 6gnos over the year. So you got taxed at 35% all year on your 60K salary (60000 * 0.35 = 21000). Now that 21K is already giggity goooone, but you deduct your 6K that you contributed to your RRSP and your “taxable” income is only (60K-6K = 54K). The taxes on this are then (54K * 0.35 = 18900) so a diff of (21000-18900 = 2100)….. which gets sent back to your hot little hands. This effect is larger the more money you make and the higher tax bracket you are in, however there are limits to the amount you can contribute each year. K I’ll pause while everyone goes to brush their teeth after vomming from all those numbers savagely forcing themselves into eachother in front of your eyes. It was a necessary evil, trust a brotha.

So it’s 40 years later and you’re a wise powerful wealthy women. You’ve retired your sexy tax glasses for sexy tax robot eyes and you are ready to wrap it up and retire yourself. You’ve racked up a ton of paperz in your RRSP account and now, since you no longer technically have any income your tax bracket is way down at the lowest amount. The second way RRSPs help you out is to allow you to withdraw from your account at this new, way lower tax bracket. Essentially what you are doing with an RRSP is deferring paying tax on your income from now, when you make pooploads of money and are taxed a ton on it, to later when you are making no money and just pooping loads. Plus your money is growing the whole time (tax free as well!) you are saving it. RRSPs make sense for people saving long term who are in a high tax bracket.

Next we have the brand spankin' new Tax Free Savings Account (TFSA), which in essence does the opposite of the RRSP. So now you are a nubile young student making 20K a year part time sassing unnecessary cellphones into the pockets of the elderly. You are getting taxed practically nothing to start cause you are so damn poor and anything you do get taxed you get back due to tuition credits (which reduce your income similar to the RRSP contributions above). So all your earnings now are pretty much tax free, or at least very lightly taxed, and so you put just a smidge away monthly in a TFSA. So this money grows, you grow up and get a big boy job, and start getting the shit taxed out of you, luckily for you you got this nice little lump saved up in this account that you can pull out at any time and not get taxed on because you already got taxed on it when you were a kid making dick all.

To wrap it up, you’re gonna get taxed. Deal with it. But, if you’re a student getting coddled before having lubeless tax sex done to you later in life, stuff some of your money in a TFSA and have it grow tax free for bonus money time later in life. If you are already deep into the tax Slave/Master dynamic, start getting a bit of your dignity back by putting your cashish into an RRSP and bustin’ it out later in life when things are much….. gentler.

Well it goes like this; you go to work with your lunchpail and your short sleeved dress shirt, stuff yourself in your work box, chuckle at Dagwood Bumstead's latest antics, slang some mild sexual harassment at the sultry new secretary, go to the women’s washroom and talk about feelings n’ shit, try to break the glass ceiling, and bring home the bacon cause you are a strong independent lioness woman! You get your bi-weekly paycheque ($2,500 from $60,000 annually), the government hops in and hustles 35% in a canvas sack with a dollar sign on it ($875) and boom bam baby it’s saving time with the rest ($1,625). After paying off your monthly installment on the platinum edition sex swing, you toss $250 into a well diversified RRSP filled with ETFs and sit back feeling pretty damn good about yourself…. So where the shit are the tax advantages you should be asking yourself at this point?

Well my friend, when tax season rolls around at the end of the year and you are crushing wine and filling out your taxes with your sexy tax glasses on, you get to deduct all that money that you put into your RRSP from your annual taxes. So, break out your abbacus, say you paid off the swing and were able to maintain contributing $250 every two weeks, so $500 a month * 12 months = 6gnos over the year. So you got taxed at 35% all year on your 60K salary (60000 * 0.35 = 21000). Now that 21K is already giggity goooone, but you deduct your 6K that you contributed to your RRSP and your “taxable” income is only (60K-6K = 54K). The taxes on this are then (54K * 0.35 = 18900) so a diff of (21000-18900 = 2100)….. which gets sent back to your hot little hands. This effect is larger the more money you make and the higher tax bracket you are in, however there are limits to the amount you can contribute each year. K I’ll pause while everyone goes to brush their teeth after vomming from all those numbers savagely forcing themselves into eachother in front of your eyes. It was a necessary evil, trust a brotha.

So it’s 40 years later and you’re a wise powerful wealthy women. You’ve retired your sexy tax glasses for sexy tax robot eyes and you are ready to wrap it up and retire yourself. You’ve racked up a ton of paperz in your RRSP account and now, since you no longer technically have any income your tax bracket is way down at the lowest amount. The second way RRSPs help you out is to allow you to withdraw from your account at this new, way lower tax bracket. Essentially what you are doing with an RRSP is deferring paying tax on your income from now, when you make pooploads of money and are taxed a ton on it, to later when you are making no money and just pooping loads. Plus your money is growing the whole time (tax free as well!) you are saving it. RRSPs make sense for people saving long term who are in a high tax bracket.

Next we have the brand spankin' new Tax Free Savings Account (TFSA), which in essence does the opposite of the RRSP. So now you are a nubile young student making 20K a year part time sassing unnecessary cellphones into the pockets of the elderly. You are getting taxed practically nothing to start cause you are so damn poor and anything you do get taxed you get back due to tuition credits (which reduce your income similar to the RRSP contributions above). So all your earnings now are pretty much tax free, or at least very lightly taxed, and so you put just a smidge away monthly in a TFSA. So this money grows, you grow up and get a big boy job, and start getting the shit taxed out of you, luckily for you you got this nice little lump saved up in this account that you can pull out at any time and not get taxed on because you already got taxed on it when you were a kid making dick all.

To wrap it up, you’re gonna get taxed. Deal with it. But, if you’re a student getting coddled before having lubeless tax sex done to you later in life, stuff some of your money in a TFSA and have it grow tax free for bonus money time later in life. If you are already deep into the tax Slave/Master dynamic, start getting a bit of your dignity back by putting your cashish into an RRSP and bustin’ it out later in life when things are much….. gentler.

Thursday, September 2, 2010

Why you shouldn’t take stock tips from BNN, CNBC, Jim Cramer’s Mad Money, your taxi driver, your friend who understands finance, or the guy who sexually abuses hair gel at the gym.

“Yo guy, GUY, bro, guy, broguy, I’m telling you guy, you gotta buy Apple. The iPhone maaannnnnn, the iPhone is killing it! Before it was at 100 now it’s down at 60 it’s for surezies goin back to 100 bro.” That took me like 15 minutes to type ‘cause I kept having to go vom during it. You hear this type of shit everyday; at the gym, on TV, on google ads, on finance sites, at your local crack den, etc. It’s the belief that because of ONE specific thing THIS specific stock is going to go to THIS specific value stamped it no erasies.

Stocks are not like math equations, chemistry, or “blowjob?” meaning there is no definite answer and this kind of absolutism is absurd. Everyone is making an educated guess at the “underlying value” of a stock that is influenced by a bajillion factors from; interest rates and investor sentiment to inflation, prices of inputs like oil (ISBA: Factor prices), foreign and domestic economy, debt crises overseas, and on and on and on. Bottom line: unless you have inside information or are manipulating the market it is impossible to know with confidence what any given stock is going to do. The best someone can possibly do is: “based on these factors, holding everything else constant, if the market responds normally, this stock MAY go to this price eventually.”

Yaaawwwwwwn. Who the shit is going to click on a link that says “possible slightly above average gains if market predictions are accurate and all other factors remain constact” when they can click on a link that says “THIS STOCK IS GOING UP 1000% GUARANTEED !! SECRET FORMULA!! BEAT WALL STREET!! FREE HANDYS FROM HOT CHIXXX!!” The point is that responsible financial analysis with a discussion of the downside risks doesn’t sell, guarantees, promises, and healthy doses of unsubstantiated shaiza sell.

There is a theory out there that many of the financial equations and subsequent theories are based on that is called the theory of market rationality…hey HEY! WAKE UP! Theory time will be quick I promise. This theory says that the market is made up of perfectly rational people investing perfectly rationally, everyone is perfectly diversified and taking the exact amount of risk they can handle, and if something changes with a company or economy the market will adjust to it gradually in a perfectly rational manner………. WTF? Instead what we see in the market looks like Tortuga in the 17th century, just pirates swingin off chandeliers everywhere,swearing and pillaging shit. If they even catch a glimpse of rationality you better believe it’s gonna be raining fists all up in this humpty bumpty. So what do these swarthy fellows in the market mean for you? You could have the best researched plan in the world, know the shit out of the fundamentals for a stock, have done a complete macroeconomic analysis, pick your exit strategy, tip toe into the market and “YAAARRRRRRRR”….. you’re fucked, because of something completely out of your control that you or anyone else could never have seen coming.

I paint a grim picture to illustrate a point; the market can stay irrational and fucked up longer than you can stay solvent. There are no shortcuts in investing, if it seems too good to be true it is. Stay away from investing based on advice from chuckys who haven’t done their research. Even if it’s a “financial reporter” or whatever on BNN or CNBC, look at the company yourself before doing anything don’t take their word for it. There is no reason for buying that can be explained fully in 5 minutes. If anyone truly did have a miracle stock, why the hell would they tell you about it? If you don’t have the financial wherewithal to at least basically evaluate a company yourself then DON’T PICK STOCKS. Stay diversified, invest long term, and for god’s sake tell that greaser at the gym to shooosh about Apple….. or just think about it and tell people you did afterwards….he is pretty jacked….

Stocks are not like math equations, chemistry, or “blowjob?” meaning there is no definite answer and this kind of absolutism is absurd. Everyone is making an educated guess at the “underlying value” of a stock that is influenced by a bajillion factors from; interest rates and investor sentiment to inflation, prices of inputs like oil (ISBA: Factor prices), foreign and domestic economy, debt crises overseas, and on and on and on. Bottom line: unless you have inside information or are manipulating the market it is impossible to know with confidence what any given stock is going to do. The best someone can possibly do is: “based on these factors, holding everything else constant, if the market responds normally, this stock MAY go to this price eventually.”

Yaaawwwwwwn. Who the shit is going to click on a link that says “possible slightly above average gains if market predictions are accurate and all other factors remain constact” when they can click on a link that says “THIS STOCK IS GOING UP 1000% GUARANTEED !! SECRET FORMULA!! BEAT WALL STREET!! FREE HANDYS FROM HOT CHIXXX!!” The point is that responsible financial analysis with a discussion of the downside risks doesn’t sell, guarantees, promises, and healthy doses of unsubstantiated shaiza sell.

There is a theory out there that many of the financial equations and subsequent theories are based on that is called the theory of market rationality…hey HEY! WAKE UP! Theory time will be quick I promise. This theory says that the market is made up of perfectly rational people investing perfectly rationally, everyone is perfectly diversified and taking the exact amount of risk they can handle, and if something changes with a company or economy the market will adjust to it gradually in a perfectly rational manner………. WTF? Instead what we see in the market looks like Tortuga in the 17th century, just pirates swingin off chandeliers everywhere,swearing and pillaging shit. If they even catch a glimpse of rationality you better believe it’s gonna be raining fists all up in this humpty bumpty. So what do these swarthy fellows in the market mean for you? You could have the best researched plan in the world, know the shit out of the fundamentals for a stock, have done a complete macroeconomic analysis, pick your exit strategy, tip toe into the market and “YAAARRRRRRRR”….. you’re fucked, because of something completely out of your control that you or anyone else could never have seen coming.

I paint a grim picture to illustrate a point; the market can stay irrational and fucked up longer than you can stay solvent. There are no shortcuts in investing, if it seems too good to be true it is. Stay away from investing based on advice from chuckys who haven’t done their research. Even if it’s a “financial reporter” or whatever on BNN or CNBC, look at the company yourself before doing anything don’t take their word for it. There is no reason for buying that can be explained fully in 5 minutes. If anyone truly did have a miracle stock, why the hell would they tell you about it? If you don’t have the financial wherewithal to at least basically evaluate a company yourself then DON’T PICK STOCKS. Stay diversified, invest long term, and for god’s sake tell that greaser at the gym to shooosh about Apple….. or just think about it and tell people you did afterwards….he is pretty jacked….

Subscribe to:

Posts (Atom)